Anthropic First Profitable Quarter: $10.9B Revenue

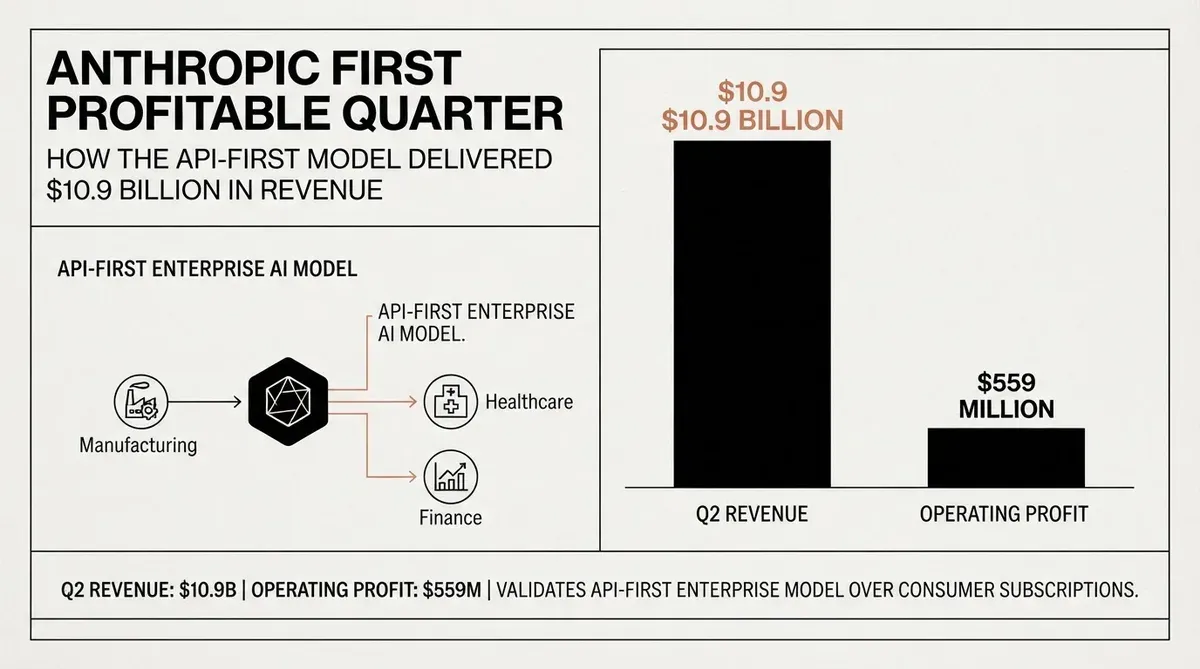

Anthropic has achieved its first profitable quarter with a projected $10.9 billion in Q2 2026 revenue and an operating profit of approximately $559 million, validating the argument that an API-first enterprise strategy can sustain foundation-model economics better than a consumer subscription model. The company informed investors that revenue more than doubled from the $4.8 billion reported in Q1, according to sources with knowledge of the figures.

The milestone lands roughly two years ahead of Anthropic's own internal projections. The company's annualized revenue run rate now stands at approximately $43.6 billion, and its private market valuation has topped $1.2 trillion, placing it ahead of OpenAI on that metric. Salesforce required about 20 years to generate $30 billion in annual revenue. Anthropic is nearly at that level after fewer than three years of commercial operations.

Claude Code Is the Growth Engine

The primary driver behind the revenue acceleration is Claude Code, the agentic coding tool that has become Anthropic's fastest-growing product. Claude Code powers more than 7% of all GitHub commits and went from zero to a $2.5 billion annualized run rate within nine months of launch. By May 2026, that figure had reached roughly $8 billion in annualized revenue. Programming use cases now account for the single largest revenue category for the company.

Eight of the Fortune 10 are Anthropic customers. This concentration of high-value enterprise relationships produces recurring revenue with lower churn and higher per-customer contract values than a consumer subscription base. Net-new ARR added each month climbed from $3 billion in January 2026 to $11 billion in March, reflecting how quickly enterprises expand their usage once they commit to the platform. Total annualized recurring revenue has increased from roughly $9 billion to over $60 billion across recent quarters.

The contrast with OpenAI's business model is instructive. OpenAI has leaned heavily on ChatGPT Plus subscriptions and consumer brand marketing, which carry higher customer acquisition costs and more churn sensitivity. Anthropic sells API access and coding tools directly to developers and engineering organizations, creating a usage-based revenue model where spending scales automatically as teams integrate Claude deeper into their workflows. The enterprise focus also means that budget decisions are made at the organizational level, where contracts run longer and expansion is driven by team adoption rather than individual renewal choices.

The Margin Turnaround

Anthropic's gross margin recovery from negative territory to 65% is one of the most dramatic operational improvements in recent software history. Gross margins were as low as -94% during the heavy infrastructure build phase, when the company was spending massively on compute without the revenue base to offset it. The recovery reflects optimized inference infrastructure, larger and more efficient model architectures, and the fixed-cost leverage of running a high-utilization compute fleet. Each generation of Claude models delivers more tokens per dollar of compute, creating a natural margin expansion cycle that should persist across future model iterations.

The company projects GAAP EBIT of over $1 billion by Q3 2026, meaning the $559 million Q2 operating profit is likely the start of a sustained profitability trend rather than a one-quarter anomaly. For the full calendar year, analysts estimate Anthropic will generate between $20 billion and $26 billion in revenue, which would place it among the top five software companies globally by revenue, behind only Microsoft among pure software firms.

This trajectory outpaces the pre-IPO revenue growth of both Google and Facebook. Zoom, often cited as one of the fastest-growing enterprise SaaS companies in history, reached roughly $623 million in quarterly revenue at its growth peak. Anthropic is projecting more than 17 times that figure in Q2 alone. The comparison underscores how the AI market's total addressable opportunity differs fundamentally from prior software categories, but it also highlights the unique economics of API-based consumption models where customers pay per token rather than per seat.

Talent Acquisition Signals Ambition

Anthropic has added three high-profile hires in the past nine weeks. Andrej Karpathy, who previously led AI at Tesla and co-founded the computer vision group at OpenAI, joined the pretraining team. John Jumper, a Nobel laureate recognized for leading the AlphaFold project at DeepMind, also left Google for Anthropic. Tom Blomfield, the Monzo co-founder and former Y Combinator executive, joined the compute infrastructure team. These appointments suggest Anthropic is investing aggressively in next-generation model architecture and the infrastructure needed to train and serve it at scale, rather than resting on current revenue momentum. The hires also signal to the talent market that Anthropic is the destination of choice for AI researchers seeking both scientific impact and financial stability.

The timing of these hires matters. All three joined within a nine-week window during a quarter when the company was simultaneously projecting its first operating profit. That pattern suggests Anthropic is using its financial momentum as a recruiting asset, converting revenue credibility into talent that can sustain the technical lead. The compute team addition in particular indicates that Anthropic views infrastructure efficiency as a durable competitive moat, not a short-term cost to optimize.

Anthropic First Profitable Quarter Proves API-First Model

Anthropic's financial results carry implications beyond the company itself. The Anthropic first profitable quarter demonstrates that the foundation-model business can achieve sustainable economics when the product is embedded directly into professional workflows as infrastructure rather than packaged as a consumer subscription. The API pricing model allows developers to start spending immediately with no sales cycle. Claude Code's agentic capabilities create an expansion loop where increased usage drives further integration, making the tool more essential over time.

This stands in contrast to the consumer subscription model where growth depends on marketing spend, feature-driven retention, and price sensitivity at the individual user level. Enterprise API revenue benefits from budget expansion cycles, multi-year commitments, and the network effects of team-wide adoption. The gross margin trajectory confirms that as model efficiency improves, the unit economics of API delivery get better, not worse, creating a natural operating leverage that consumer subscription models cannot match as easily.

OpenAI has acknowledged this dynamic. The company has been expanding its enterprise sales team and launching tiered API pricing, but its revenue base remains heavily weighted toward consumer subscriptions. Anthropic's financial results put pressure on OpenAI to demonstrate that its own model can achieve similar unit economics at comparable scale. The divergence in business models between the two leading AI firms will become one of the defining strategic questions for investors evaluating which company offers better long-term margin potential.

Private market investors have already voted. Anthropic's valuation exceeding $1.2 trillion and surpassing OpenAI reflects confidence that the API-first approach will sustain higher margins and lower churn over time. If the company maintains its current trajectory, an IPO would rank among the largest in technology history, with potential implications for how the market prices AI companies going forward. The $900 billion pre-money valuation from the most recent fundraising round now looks conservative against the current revenue run rate of over $43 billion annualized, a ratio that would be rare in traditional enterprise software.

Why this matters

Anthropic's first profitable quarter rewrites the economic narrative around foundation-model companies. Where skeptics argued that AI firms would remain dependent on venture capital indefinitely, Anthropic has demonstrated that an enterprise-focused, API-first strategy can generate real operating profits at scale. For CTOs and engineering leaders evaluating AI vendors, the implication is that platform stability and long-term viability are now tied to a sustainable business model, not subsidized pricing. The key question is whether Anthropic can maintain the 65% gross margin trajectory as the next generation of more capable models demands higher compute investment. If it can, the API-first enterprise model will become the template for how AI companies achieve profitability in a capital-intensive industry.

AI-generated image.

Related Articles

- Anthropic Surpasses OpenAI in U.S. Enterprise AI Adoption as Revenue Targets Surge

- AI Revenue Growth Hits New Heights as OpenAI and Anthropic Reach Q1 Milestones

- Anthropic Valuation Hits $900 Billion as Firm Surpasses OpenAI in New Funding Round

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.