South Korea Semiconductor Investment Hits $648B

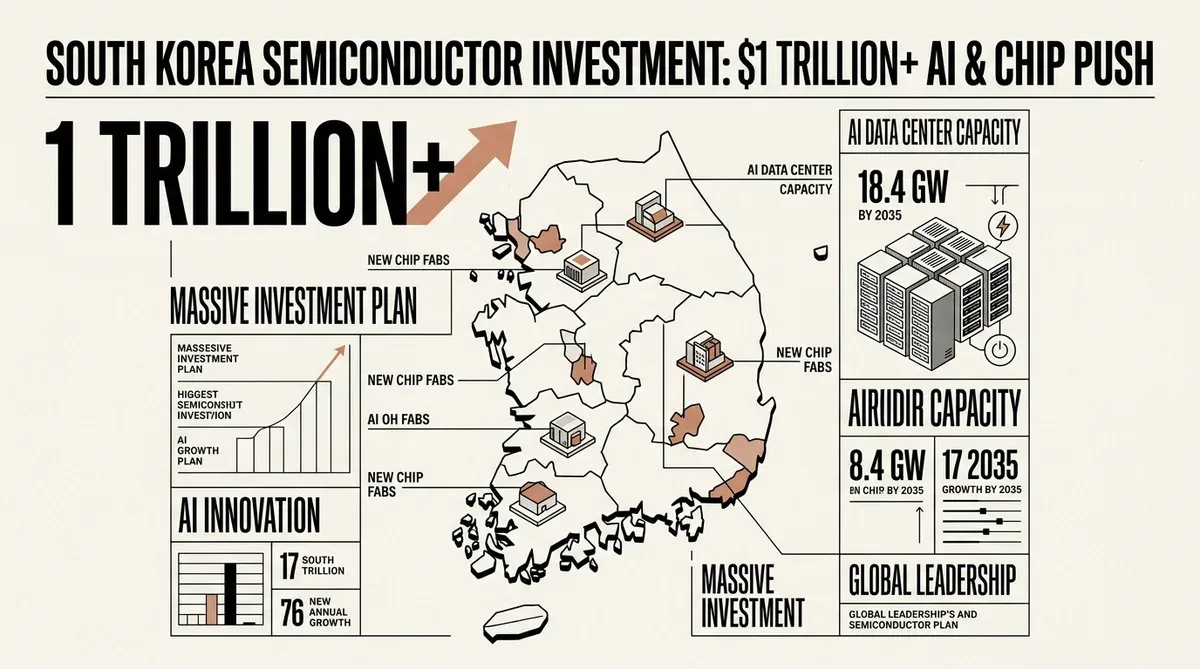

South Korea's South Korea semiconductor investment plan, exceeding 1,000 trillion won (about $648 billion), directs funds into semiconductor fabrication, AI infrastructure, and data centers. President Lee Jae Myung announced the strategy on June 29, 2026, describing it as a race to secure core AI components faster than global competitors.

The initiative rests on three areas: semiconductors, physical AI, and data center infrastructure. Samsung Electronics and SK Hynix, the world's two largest memory chipmakers, are the main private backers. Lee outlined a program that combines government coordination with corporate capital.

South Korea Semiconductor Investment Breakdown

Samsung and SK Hynix together will contribute 800 trillion won (about $518 billion) to build four new chip fabrication sites in southwestern South Korea. Samsung will build its cluster in Gwangju. SK Hynix is still finalizing its site. Local governments in Gwangju and South Jeolla province will add 5 trillion to 20 trillion won ($3.2 billion to $13 billion) in support.

A separate 81 trillion won ($52.5 billion) chip-packaging cluster is planned for the Chungcheong area. It will focus on advanced packaging for high-bandwidth memory (HBM) and other chip architectures. HBM is a key component in AI systems, where memory bandwidth affects model training and inference speed.

On the data center side, the government aims to add 10 gigawatts of AI data center capacity by 2035, raising the national total to more than 18.4 GW. The expansion addresses the power demands of large-scale AI workloads and positions South Korea as a potential compute hub for the Asia-Pacific region.

Private Sector Commitments

Beyond the chipmakers, SK Group, GS Group, and Naver have committed 550 trillion won ($356 billion) in private backing for the broader initiative. The combined South Korea semiconductor investment across all pillars exceeds 1,000 trillion won (roughly $648 billion) and is directed at data centers, AI infrastructure, and semiconductor production.

The strategy also targets a doubling of DRAM production within five years. DRAM is a foundational component for AI servers; each GPU accelerator requires substantial high-bandwidth memory capacity. AI training clusters now consume memory at rates that were unimaginable a few years ago.

Strategic Rationale

The South Korea semiconductor investment is a response to intensifying global competition in AI infrastructure. The United States, China, and the European Union have announced large-scale chip and AI programs in recent years. South Korea's plan is a bid to prevent its memory chip industry from falling behind rivals that are investing in fabrication capacity and packaging technology.

Placing new fabrication sites in the southwest and Chungcheong areas, rather than in the Seoul metropolitan region, also aims to address regional economic imbalances. Industry experts warn that this diversification will require solving challenges in skilled labor and logistics infrastructure. The southwestern regions are less industrialized, and parallel investment in transportation, housing, and workforce training is needed.

High-bandwidth memory is a central part of the strategy. The technology stacks DRAM dies vertically to maximize data throughput. Samsung and SK Hynix have competing HBM product lines. The investment plan ensures South Korean manufacturers maintain production capacity for several generations of HBM standards. The packaging cluster in Chungcheong is designed to keep HBM production vertically integrated within South Korea.

Global AI Market Implications

The scale of the South Korea semiconductor investment reshapes the supply-side dynamics of the global AI chip market. With four new fabrication sites and a dedicated packaging cluster coming online over the next decade, the country is positioned to supply a significant share of the world's AI memory and logic chips. For AI companies and hyperscalers building data center capacity, the plan indicates that HBM supply will remain concentrated among South Korean manufacturers.

The 18.4 GW data center target also has implications for energy markets. Powering AI workloads at that scale requires stable, high-capacity electricity generation. The plan emphasizes untapped power resources in the southwest, suggesting a coordinated approach to energy infrastructure alongside chip production. This integrated planning, aligning power generation, chip fabrication, packaging, and data center construction in the same regions, is a model few other countries have attempted at this scale.

For business leaders and technology strategists, the initiative offers several takeaways. Companies that depend on HBM or DRAM supply should expect South Korean manufacturers to maintain or extend their lead in memory technology over the next five years. The doubling of DRAM production capacity could moderate pricing pressure, though AI demand growth may absorb much of that supply. The emphasis on physical AI — integrating capabilities into robots, manufacturing equipment, and infrastructure — points to a downstream market where South Korean companies will compete aggressively.

The plan also creates competitive pressure on chipmakers in Taiwan, the United States, and Europe, who now face a well-funded, government-backed expansion from South Korea's memory duopoly. The combination of scale, government coordination, and vertical integration from chip design to data center operation gives Seoul a structural advantage that rivals will find difficult to match without similar national commitments. Taiwan's TSMC, which dominates logic chip fabrication, now confronts a South Korean strategy that invests heavily in the memory and packaging layers of the AI stack, areas where TSMC has less direct exposure.

The broader implication is that national industrial policy is becoming a decisive factor in AI competitiveness. South Korea's approach pairs state-level coordination with private-sector execution, blending the US market-driven system with the centralized planning seen in China. For companies in the AI supply chain, understanding which regions are making these long-term capital commitments is becoming as important as tracking the technology roadmaps of individual chipmakers.

AI-generated image.

Related Articles

- Samsung Achieves Record Financial Performance as AI Semiconductor Demand Surges

- Samsung AI Chip Demand Drives $1 Trillion Valuation and $26 Billion Labor Deal

- ASE and WUS Invest NT$35 Billion in Taiwan AI Chip Packaging Plant

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.