AI Startup Funding Record 2026 Hits $392 Billion

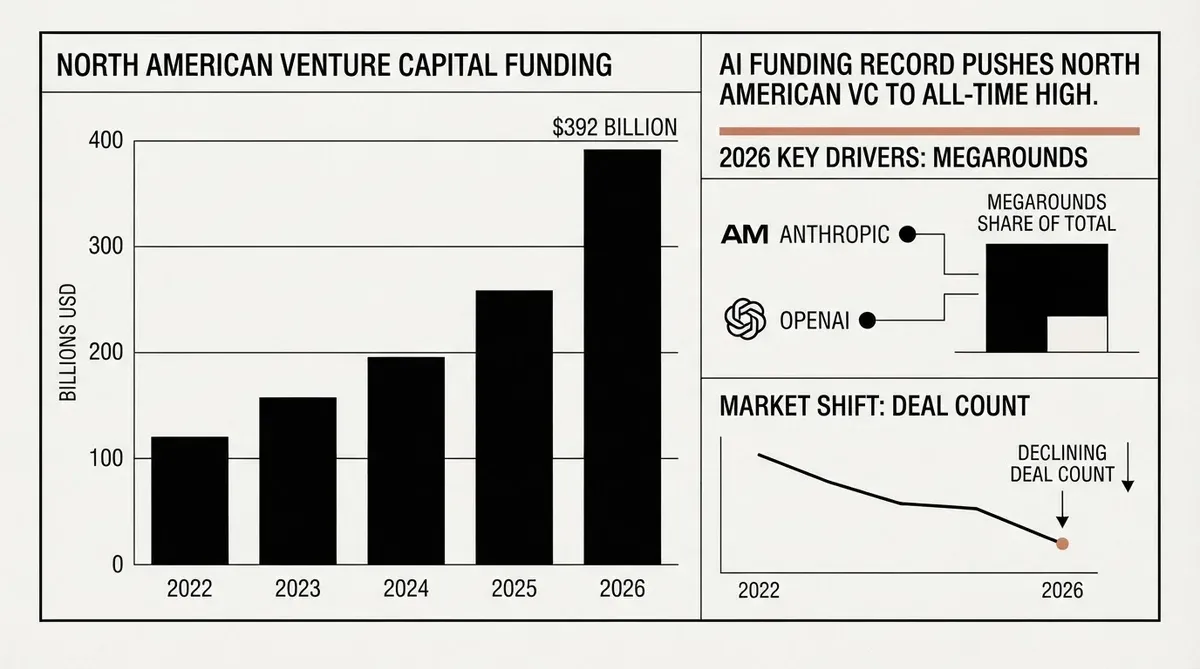

The concentration of capital among a small group of artificial intelligence leaders pushed North American startup funding to an AI startup funding record 2026 of $392 billion in the first half of 2026, according to Crunchbase data covering US and Canadian ventures. The figure reflects a market where a handful of giant rounds, rather than broad-based deal activity, drove the total beyond any prior period. The gap between total dollars and deal count reveals where the venture industry is placing its biggest bets and exposes a structural shift in how capital moves through the innovation economy.

Crunchbase reported this month that the H1 2026 total was built on two quarters that each broke records in distinct ways. The first quarter saw OpenAI close its historic fundraising round, setting a benchmark that few companies can match. The second quarter added $137.2 billion in investment, the second-highest quarterly total ever recorded, powered largely by Anthropic's massive financing, which accounted for roughly half of the Q2 figure. SpaceX contributed to the quarter's momentum with the largest initial public offering in history, followed by its acquisition of Cursor in what ranks as a record-setting startup M&A deal. Together, these transactions created a quarterly total that exceeded any prior year's single quarter except the one immediately before it.

The $137.2 billion Q2 figure is particularly instructive because it shows how dependent the current cycle is on a small number of actors. Remove Anthropic's round, and the quarter drops to roughly $68.6 billion in identifiable large-deal activity, a figure that, while still strong by historical standards, would not have drawn the same headlines. This dependency creates a fragile structure: a single company's fundraising timeline can swing quarterly totals by tens of billions of dollars.

The AI Startup Funding Record 2026 Hides a Concentration Problem

While the headline $392 billion figure signals a booming ecosystem, the underlying metrics point to a narrowing of opportunity that has implications for founders, limited partners, and corporate development teams. Deal count remained well below the highs of prior funding cycles, meaning the same or fewer companies received dramatically more money. Late-stage megarounds exceeding $100 million consumed the vast majority of capital, leaving early-stage companies competing for a smaller share than the aggregate numbers suggest.

The implications for founders and investors are significant. When a single company like Anthropic captures roughly half of a quarter's total venture investment, it distorts the signal that aggregate funding data sends to the broader market. For limited partners evaluating venture fund performance, a few outlier rounds can mask underlying weakness in portfolio diversity. The AI startup funding record of 2026 may look like a sign of health from a distance, but on the ground it reflects a market where capital allocation is increasingly lopsided and where the gap between the top tier of AI companies and everyone else continues to widen.

Early-stage investment did rise in the second quarter, with AI again serving as the primary catalyst. The magnitude of the increase was modest compared to the late-stage surge, and the gap between early and late suggests that investors are doubling down on proven AI winners rather than spreading bets across a wide field of experimental companies. For early-stage founders outside of AI, the environment is arguably more challenging now than it was during the 2022-2023 downturn, because the sheer volume of capital flowing into AI megacompanies creates a gravitational pull that draws attention, talent, and deal flow away from other sectors.

What the Megarounds Mean for the AI Supply Chain

The dominance of AI infrastructure and model companies in the 2026 funding cycle has consequences that ripple beyond the startups themselves. OpenAI and Anthropic require enormous capital reserves to fund compute costs, talent acquisition, and the long research timelines required for frontier model development. Their ability to raise at scale creates a structural advantage that makes it difficult for smaller AI labs to compete on the same playing field. When capital is this concentrated, the competitive dynamics of the AI industry begin to resemble those of the semiconductor industry, where a few players control the majority of investment and capacity.

SpaceX's record IPO and subsequent Cursor acquisition added a second dimension to the Q2 story. The deal demonstrated that large technology acquirers are willing to pay premium prices for AI-enabled tools, even as the broader M&A market remains subdued by historical standards. Cursor, an AI coding assistant, is a category that has attracted intense interest from both venture investors and corporate buyers. This pattern could accelerate consolidation in the developer tools space, where well-funded incumbents acquire AI-native startups to bolt on capabilities rather than build them internally.

For corporate strategists evaluating the 2026 funding environment, the key takeaway is that the cost of entry in frontier AI continues to rise. Companies that have not yet secured their position in the AI stack, whether through internal development, strategic partnerships, or acquisition, face an increasingly concentrated supplier base and a narrowing window to act at reasonable valuations. The megaround cycle also pressures public market investors who may eventually be asked to absorb these companies through IPOs or direct listings at valuations that reflect private-market exuberance rather than public-market fundamentals.

From a macroeconomic perspective, the AI startup funding record 2026 of $392 billion is striking in its magnitude but revealing in its composition. The data suggests that the venture capital industry is reorganizing around a thesis that a small number of AI platforms will capture most of the value created in the current technological cycle. Whether that bet pays off depends on whether the current generation of frontier models translates into sustainable revenue and profit, a question that remains open as of mid-2026. If the returns materialize, the concentration will have been an efficient allocation of capital. If they do not, the correction could be severe precisely because so few companies absorbed so much money.

Why This Matters

The record venture investment in North America signals that institutional capital has made a decisive bet on AI as the defining technology of the decade, but the concentration of that capital carries genuine risk for the innovation ecosystem. For decision-makers across technology and finance, the H1 2026 funding data is less a celebration of abundance than a warning about dependence on a narrow set of outcomes. The lesson for strategists is that diversification remains the first principle of risk management, even in a market that appears to reward concentration, and that the true test of this funding cycle will come when the current cohort of AI leaders must demonstrate that their valuations correspond to durable business models.

AI-generated image.

Related Articles

- Anthropic Valuation Hits $900 Billion as Firm Surpasses OpenAI in New Funding Round

- AI Revenue Growth Hits New Heights as OpenAI and Anthropic Reach Q1 Milestones

- Menlo Ventures AI Investments Hit $3 Billion

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.