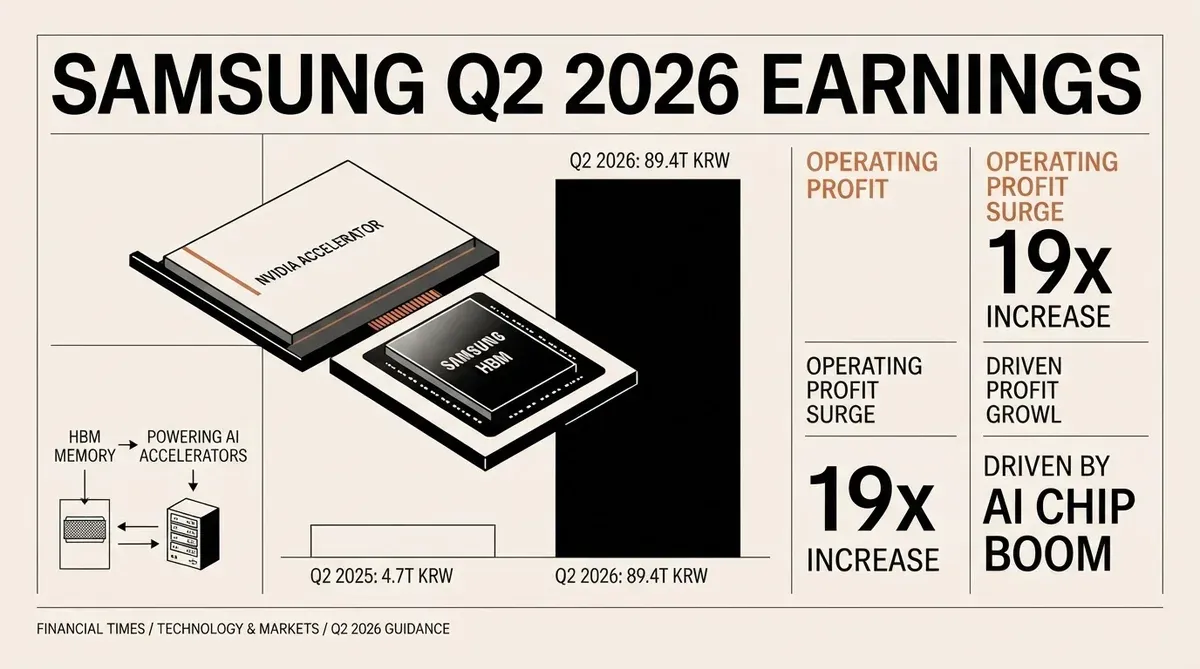

Samsung Q2 2026 Earnings: 89.4 Trillion Won on AI Chip Boom

The Samsung Q2 2026 earnings guidance, released on July 7, shows an estimated operating profit of 89.4 trillion Korean won, a roughly 19-fold increase from the 4.68 trillion won a year earlier. The company also projected consolidated sales of approximately 171 trillion won for the quarter ending June 30.

The figures, reported under Korean International Financial Reporting Standards, are the medians of Samsung's estimate ranges as required by Korean disclosure regulations. The Q2 2026 performance is a 56% sequential jump in operating profit from the 57.23 trillion won Samsung reported in Q1 2026, while sales grew from 133.87 trillion won. Year over year, revenue more than doubled from 74.57 trillion won.

AI Memory Chips Fuel Samsung Q2 2026 Earnings Growth

The explosive earnings growth traces directly to surging demand for high-bandwidth memory (HBM) chips used in NVIDIA's AI accelerators and other data center hardware. Samsung has positioned itself as a major supplier in the AI semiconductor supply chain, competing with SK Hynix for NVIDIA's HBM procurement contracts. The Samsung Q2 2026 earnings guidance confirms that the AI chip boom continues to reshape the memory industry's financial profile.

HBM chips stack multiple DRAM dies vertically to deliver the bandwidth required for training and running large language models. As hyperscale cloud providers and enterprises rush to deploy AI infrastructure, demand for these specialized memory components has outpaced general market trends for traditional DRAM and NAND flash products. Samsung's memory business, which accounts for a substantial portion of the company's overall profit, appears to have captured a large share of this premium segment.

The market for HBM is projected to grow from roughly $4 billion in 2023 to more than $25 billion by the end of 2026, according to industry estimates cited by multiple semiconductor analysts. Samsung's ability to ship HBM3E in volume during the first half of 2026 has been a critical factor in its revenue acceleration. The company has also begun sampling HBM4 with select customers, positioning for the next product cycle.

Sequential Momentum Signals Acceleration

The sequential growth from Q1 to Q2 2026 is especially noteworthy. Operating profit rose by more than 32 trillion won in a single quarter, indicating that the AI chip demand cycle is accelerating rather than plateauing. Q1 2026 already represented a strong recovery quarter for Samsung, and the Q2 guidance shows the company building on that momentum.

Revenue growth tells a similar story. The increase from 133.87 trillion won in Q1 to an estimated 171 trillion won in Q2 is a roughly 28% quarter-over-quarter gain. At an annualized run rate, Samsung's second-half 2026 sales could approach 200 trillion won per quarter if current trends continue. The company's memory division alone may be generating revenue at a pace that rivals the entire company's top line from just two years ago.

The earnings data also carry implications for the broader semiconductor industry. Suppliers of chipmaking equipment, substrate materials, and packaging services tied to HBM production should see correlated demand. Samsung's foundry and logic chip businesses, while smaller relative to the memory division, also benefit from the elevated capital spending cycle. The company operates one of the world's most advanced semiconductor fabrication facilities in Pyeongtaek, South Korea, where it has expanded capacity specifically for HBM production.

Strategic Position in the AI Supply Chain

Samsung's ability to deliver HBM3E and next-generation HBM4 products on schedule has become a key competitive differentiator. The company's vertical integration, spanning memory design, fabrication, and advanced packaging, provides a structural advantage over rivals that must rely on third-party foundries or packaging partners. Samsung operates its own chip manufacturing facilities and packaging lines, allowing it to optimize the HBM production process end to end.

NVIDIA's sustained demand for HBM has created a three-way contest among Samsung, SK Hynix, and Micron for qualification wins and supply allocations. The operating profit surge suggests the company has secured meaningful volume commitments from AI customers, translating chip shipments into record profits. SK Hynix, which pioneered HBM and has been NVIDIA's primary supplier for earlier generations, reported its own strong results earlier this year, confirming that the rising tide is lifting multiple suppliers.

Samsung's semiconductor capital expenditure for 2026 is expected to reach approximately 60 trillion won, with a significant portion allocated to HBM capacity expansion and advanced packaging infrastructure. This spending level, if confirmed, would be the highest in the company's history and signals management's confidence in sustained AI-driven demand.

Market and Investor Implications

For investors and technology strategists, the earnings guidance reinforces several points. AI infrastructure spending remains on a steep growth trajectory, with memory components representing a bottleneck that commands premium pricing. Samsung has regained pricing power in the memory market after the cyclical downturn that depressed results through 2023 and early 2024. The scale of Samsung's profit generation is operating margin exceeding 50% based on the 89.4 trillion won profit against 171 trillion won in sales and it reflects the high-margin nature of AI-grade memory products.

Comparisons with the previous cyclical peak are instructive. During the last memory super-cycle in 2017 to 2018, Samsung's quarterly operating profit peaked at around 20 trillion won. The current quarter's 89.4 trillion won figure dwarfs that earlier record by a factor of more than four, underscoring how AI demand has structurally upgraded the memory industry's earnings capacity. The shift from commodity DRAM pricing to premium HBM pricing has effectively reclassified Samsung's memory business from a cyclical player into a structural growth story.

Risks and Other Considerations

The guidance does come with caveats. Korean disclosure rules require Samsung to report ranges rather than single-point estimates, and the final audited results may differ from the medians published today. More fundamentally, the sustainability of AI chip demand depends on continued capital expenditure by hyperscale cloud operators, any slowdown in which could compress memory prices. Companies such as Microsoft, Amazon, Google, and Meta have collectively committed more than $200 billion in AI infrastructure spending through 2027, but those budgets are not guaranteed if AI returns on investment fail to materialize at expected rates.

Geopolitical factors also warrant attention. Export controls on advanced semiconductors and manufacturing equipment could affect Samsung's ability to serve certain markets. The company maintains significant production capacity in China, and trade policy changes remain a variable for the second half of 2026. New US restrictions on chip exports to specific markets could redirect some of Samsung's customer demand or complicate its supply chain logistics.

Despite these risks, the earnings guidance is a defining moment for the company and for the AI semiconductor sector. The 19-fold year-over-year profit increase provides a concrete measure of how deeply AI adoption is reshaping the hardware industry, turning memory chips, once viewed as a cyclical commodity, into a strategic asset for the AI era. The final audited earnings, expected in late July, will offer a more detailed breakdown by business segment and geographic region.

Sources

Samsung Electronics Announces Earnings Guidance for Second Quarter 2026

AI-generated image.

Related Articles

- Samsung Achieves Record Financial Performance as AI Semiconductor Demand Surges

- Samsung AI Chip Demand Drives $1 Trillion Valuation and $26 Billion Labor Deal

- SEMIFIVE Revenue Surges 137% as Demand for Custom AI ASIC Solutions Hits Record Highs

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.