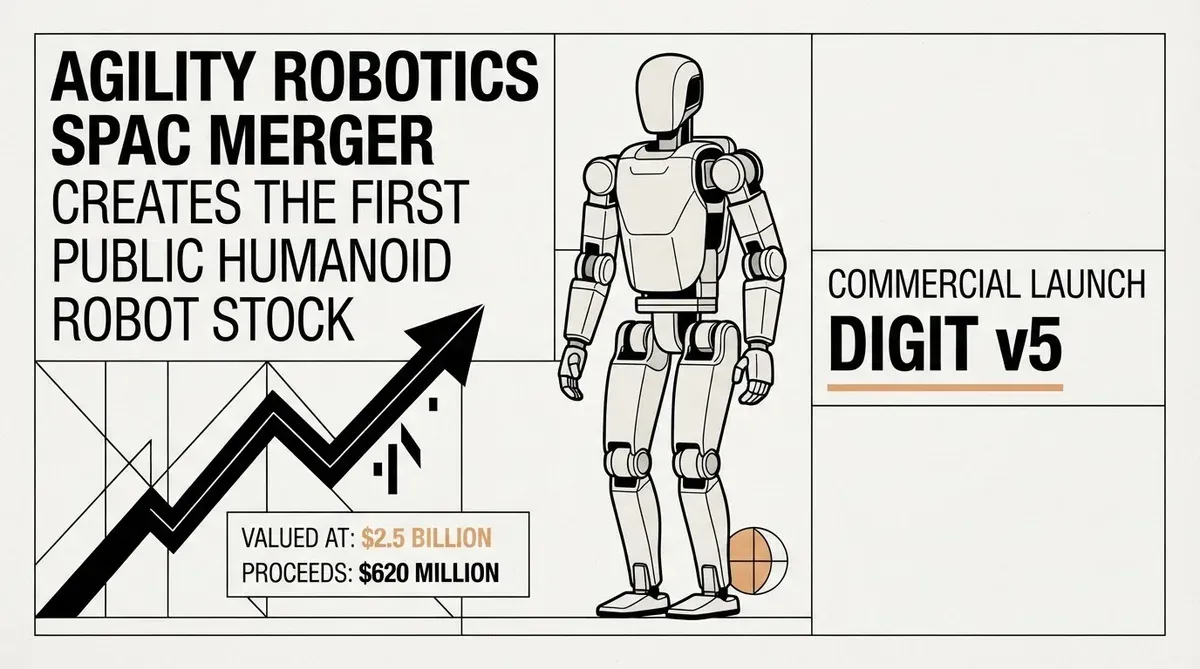

Agility Robotics SPAC Merger: First Public Humanoid at $2.5B

I have been tracking the humanoid robotics space long enough to know that the gap between demo videos and deployed robots is vast. That is why the Agility Robotics SPAC merger announced this week matters more than most headline-grabbing robotics announcements. The Oregon-based company has signed a definitive business combination agreement with Churchill Capital Corp XI, a special purpose acquisition company led by Michael Klein, in a deal that values the combined entity at $2.5 billion. When the transaction closes, Agility will become the first publicly traded pure-play humanoid robotics company on a major North American exchange.

The deal brings with it a set of financial details that are unusually concrete for this sector. According to regulatory filings, the transaction is expected to generate roughly $620 million in gross proceeds. Agility has also reported approximately $300 million in booked revenue and a deployment pipeline of about 1,000 robots. Those numbers place the company in a different category from the many robotics startups that go public with nothing but a prototype and a slide deck.

To understand why this matters, it helps to look at the broader SPAC market over the past five years. The blank-check boom of 2020 and 2021 produced dozens of electric vehicle, battery, and autonomous driving companies that merged into SPACs at valuations of $1 billion or more. Most of those stocks have since lost 80 to 90 percent of their value. Agility is making a different bet by entering the public market with booked revenue, customer contracts, and a robot that has already been deployed in production environments.

What the Digit v5 Commercial Launch Means

At the center of Agility's go-to-market strategy is Digit v5, the next-generation version of its bipedal humanoid robot. The company is now preparing for a commercial launch of this platform, which is designed specifically for logistics and industrial tasks such as box moving, palletizing, and warehouse material handling. This is not a general-purpose humanoid meant to fold laundry or load a dishwasher. The design constraints reflect a deliberate choice to go after the market where the economics already work.

Digit's form factor is instructive. The robot stands roughly five feet nine inches tall and weighs about 140 pounds, with arms that can lift payloads of up to 35 pounds. It navigates warehouse environments using a combination of onboard sensors and AI-based perception systems. Unlike wheeled robots that require modified infrastructure, Digit walks on two legs, which means it can operate in spaces designed for human workers without facility retrofits. That compatibility is a key selling point for logistics operators who cannot afford to shut down a distribution center for weeks to install conveyor belts or robotic gantries.

The focus on industrial deployment rather than consumer robotics is a point that CEO Peggy Johnson has been explicitly making. She has emphasized that the path to profitability runs through warehouses and fulfillment centers, not living rooms. I find this grounding refreshing in a space where many companies are promising humanoids in every home within a few years. Johnson, who joined Agility in 2024 after serving as CEO of JumpCloud and holding executive roles at Microsoft and Qualcomm, brings a level of operational credibility that is rare in the robotics startup world. She is making a narrower but more credible bet: that the return on investment for a robot that can work a 16-hour shift in a distribution center is calculable today, whereas the consumer use case remains years away.

Investor Signal Behind the Agility Robotics SPAC Merger

The strategic investor lineup provides another reason to take this deal seriously. The company's backers include NVIDIA, Amazon, SoftBank Vision Fund 2, Foxconn, Schaeffler, DCVC, Abico, and Playground Global. That is a cross-section of the technology, manufacturing, and logistics industries, and each of these investors brings more than capital to the table.

Amazon's involvement is particularly telling. The e-commerce and cloud computing giant has been testing Digit robots in its fulfillment network, and a deeper integration between the two companies could give Agility a distribution channel that no other humanoid robotics company can match. Amazon already operates hundreds of thousands of mobile robots in its warehouses through its Kiva and Proteus platforms, but those are wheeled systems designed for specific tasks. A bipedal humanoid that can handle the final feet of package flow (the irregularly shaped boxes, the items that fall off conveyor belts, the tasks that currently require a human picker) is a new capability layer. Similarly, Foxconn's stake signals potential applications in electronics manufacturing, where labor shortages and repetitive motion injuries create a strong economic case for automation.

NVIDIA's presence ties back to the compute platform that powers Digit's autonomy stack. The company's Isaac robotics platform and Jetson modules provide the perception and simulation infrastructure that Agility uses for training and deployment. This aligns the deal with the broader physical AI ecosystem that Jensen Huang has been describing as the next wave of artificial intelligence, where robots learn to interact with the physical world through simulation and reinforcement learning rather than hand-coded behaviors.

Schaeffler's involvement suggests the technology is being evaluated for e-commerce warehousing and heavy industrial settings alike, where precision and endurance matter. That diversification of use cases reduces the single-customer risk that would exist if Agility were dependent entirely on Amazon.

How Agility Compares to the Competition

The humanoid robotics field has become increasingly crowded over the past two years. Figure AI, backed by OpenAI, Microsoft, and NVIDIA, is developing its own general-purpose humanoid and has raised substantial venture funding at valuations that reportedly exceed $2 billion. Boston Dynamics, now under Hyundai ownership, continues to iterate on its Atlas platform. Tesla has shown prototypes of its Optimus robot and described ambitious production targets. Apptronik, 1X Technologies, and a handful of Chinese companies are also pursuing commercial humanoids.

What sets Agility apart is the combination of a deployed product and a public market path. Figure AI has shown impressive demos but has not disclosed revenue. Boston Dynamics has sold Spot quadruped robots at scale but has not commercialized a bipedal humanoid. Tesla has not delivered a working Optimus unit to a paying customer. Agility, by contrast, can point to actual deployments, customer contracts, and a balance sheet backstopped by $620 million in gross proceeds from the SPAC. That funding cushion gives the company room to scale production and absorb the inevitable setbacks that come with manufacturing complex electromechanical systems at volume.

The Financial Realities

While the $2.5 billion valuation is the number that will dominate the headlines, I think the more important figure is the $300 million in revenue that Agility has already booked. In a SPAC market that has been littered with companies that merged with blank-check vehicles only to reveal that their revenue projections were fictional, Agility arrives with actual customer contracts and a deployable product. The 1,000-robot pipeline that includes names like Amazon and Toyota provides the kind of demand visibility that most pre-IPO robotics companies cannot show.

That is not to say the deal carries no risk. SPAC mergers have a well-documented history of underperforming once the initial trading pop fades, and Agility will face the same pressure that every newly public company confronts: the need to convert a pipeline into recurring revenue and to scale production without destroying margins. Scaling humanoid robot manufacturing is an unsolved problem. No company has ever produced bipedal humanoid robots in quantities exceeding a few hundred units per year, let alone the thousands that would be required to justify a $2.5 billion valuation on fundamentals alone. Digit v5 will need to prove that it can be built reliably and cost-effectively at volumes that make the unit economics work.

There is also the question of SPAC dilution. The structure of these transactions typically involves warrants, earnouts, and sponsor promotes that reduce the effective value received by public shareholders. The $620 million in gross proceeds must be evaluated net of transaction fees, underwriting costs, and the sponsor's equity stake. Agility's investor materials will need to present a clear picture of the post-merger share count and the implied enterprise value to allow investors to make an informed assessment.

Why This Matters

The Agility Robotics SPAC merger is the first real test of whether the humanoid robotics thesis can hold up under public market scrutiny. Every other humanoid company today remains private, and the sector has been fueled by venture capital dollars betting on a future that may still be five to ten years away. Agility is putting a floor under that narrative by showing that a humanoid robotics company can generate revenue, sign customer contracts, and attract strategic investors from across the industrial economy. If Agility succeeds as a public company, it will open the door for other humanoid robotics firms to follow the same path. If it stumbles, the SPAC structure and its associated costs will amplify the damage. Either way, the outcome will define the next chapter of this industry, and strategists should be watching closely.

AI-generated image.

Related Articles

- Robseek Intelligence to List on NYSE Following $1 Billion SPAC Merger

- Humanoid Robotics IPO Hype Masks Unitree Profit Crisis

- Generalist AI Funding Round Secures $400 Million to Advance Physical AGI

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.