AI Chip Stocks Set H1 Records Then Suffer Worst Correction

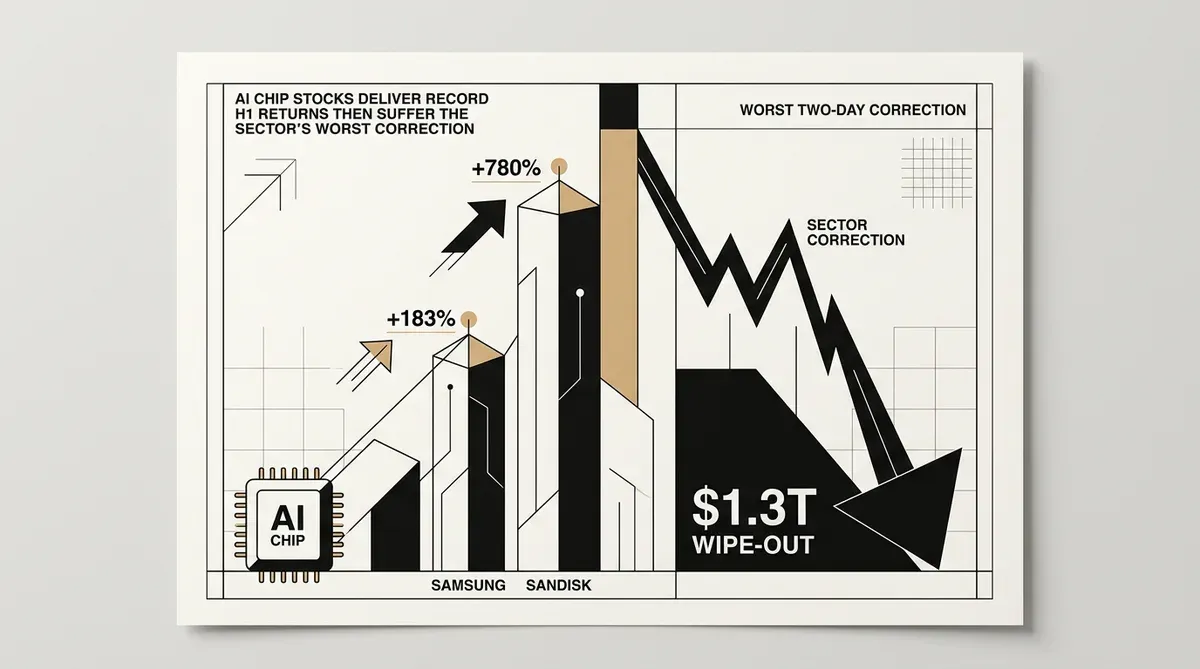

Two competing realities defined AI chip stocks in the first half of 2026. The first six months saw historic gains for semiconductor stocks. South Korean memory producers and American storage companies posted returns that beat all other major asset classes. That run ended on June 26. Over two sessions, global semiconductor stocks lost $1.3 trillion in value, the biggest two-day decline the sector has ever recorded.

South Korea's Kospi benchmark recorded its strongest first half in decades. Samsung shares more than doubled, while SK Hynix more than tripled, as both companies supply the high-bandwidth memory essential for AI training. Profit margins expanded sharply through 2026 as demand outpaced supply.

How the Rally in AI Chip Stocks Unfolded

American chipmakers saw even larger moves. Sandisk, Western Digital, Micron, and Seagate all posted share price gains that more than doubled, with some more than tripling. The Philadelphia Semiconductor Index rose for most of the period alongside the broader AI infrastructure buildout.

The surge was driven by a shift in institutional money from software giants to hardware firms. The 2026 rally differed from earlier AI booms. It was not limited to NVIDIA and a few others; it spread across memory, storage, and foundry firms as enterprise AI deployments moved from experiments into production.

Such gains mark a break from the historical pattern for semiconductor stocks. Memory and storage companies were once cyclical, moving with commodity prices. In 2026, that changed. Investors started seeing them as structural growth bets linked to AI data center spending. The market now assigns a premium to any chipmaker that can show a direct tie to data center buildout, regardless of its past as a cyclical supplier.

The Late-June Correction

The rally ended on June 26 when a sharp selloff began. Over two trading days, the global chip sector shed $1.3 trillion in market capitalization. The Philadelphia Semiconductor Index tumbled 7.9% in a single session. The Nasdaq Composite lost more than 4%. NVIDIA shares traded near $200, roughly 26% below their 52-week high of $236.26 set in May.

Rental prices for high-end GPUs fell 31% over three weeks, a sign that spot demand for AI compute may be softening. Samsung and SK Hynix each dropped more than 12% during the selloff. The correction followed a classic pattern: a rapid buildup of expectations, a shock that tests those expectations, and a valuation reset across the sector.

Despite the correction, the first-half returns remain extraordinary. The S&P 500 gained 7.4% in the same period, a respectable showing that nonetheless pales next to the semiconductor sub-sector. The Nikkei index rose 38%, driven largely by Japanese semiconductor equipment makers that supply fabrications tools for TSMC and other foundries.

The divergence between semiconductor stocks and the broader market highlights how central AI infrastructure has become to index performance. A significant portion of the S&P 500's first-half gain came from chip and hardware companies rather than the software and internet stocks that led previous bull runs.

Downstream Effects on Consumers

The memory chip price increases that powered the rally have already produced visible effects beyond financial markets. Apple raised prices on MacBooks and iPads this year, citing rising memory chip costs that flow directly from AI-driven demand for high-bandwidth memory. When the same fabrication capacity serves both AI accelerators and consumer devices, the pricing pressure carries over into end-user products.

This transmission mechanism illustrates how AI capital expenditure flows through to the broader economy. Companies building data centers bid up the price of memory and storage chips, which in turn raises costs for PC and tablet manufacturers. The cycle has no immediate end in sight, as enterprises continue to commit large portions of their IT budgets to AI infrastructure.

The consumer price effect is one of the most tangible signals that AI demand has moved beyond the purely financial domain. Hardware cost increases that begin in data center procurement end up affecting the pricing of devices sold to millions of consumers. That connection did not exist in prior technology investment cycles, where infrastructure buildout and consumer electronics pricing remained largely independent.

What the H1 Data Tells Investors

The first half of 2026 establishes several facts about the AI chip market that investors must weigh. First, demand for AI hardware is not limited to a single vendor or chip type: memory, storage, and interconnect companies all participate meaningfully. Second, the volatility inherent in the sector has not diminished; the June selloff demonstrated that even a booming market can correct violently. Third, the price effects of AI demand are now propagating beyond the data center into consumer hardware markets.

For decision-makers evaluating AI infrastructure investments, the H1 data reinforces the importance of supply chain diversification. Reliance on a narrow set of chip suppliers carries both performance risk and financial exposure. The rally and correction together suggest that the AI hardware cycle has entered a more mature phase, one where broad sector participation and periodic reassessments replace the straightforward growth story of 2023 through 2025.

The semiconductor sector enters the second half of 2026 with a valuation reset completed but the underlying demand drivers intact. Enterprise AI deployments continue to expand, cloud providers are still building out capacity, and the memory chip supply constraints that drove prices higher show no signs of easing. Whether the correction of late June proves to be a healthy pullback in a continuing bull market or the start of a deeper drawdown depends on whether AI compute demand growth can sustain the current pace of capacity expansion.

For investors tracking AI chip stocks, the June selloff has created the first real opportunity to reassess positioning since the rally began. The second half of the year will test whether the fundamental thesis that drove the H1 surge (that AI hardware demand is a multi-year structural shift rather than a speculative spike) holds under the weight of higher interest rates, export control uncertainty, and the natural lumpiness of enterprise procurement cycles.

AI-generated image.

Related Articles

- Samsung Achieves Record Financial Performance as AI Semiconductor Demand Surges

- Samsung AI Chip Demand Drives $1 Trillion Valuation and $26 Billion Labor Deal

- Intel Stock Skyrockets as AI Infrastructure Shift Drives Record Earnings Beat

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.