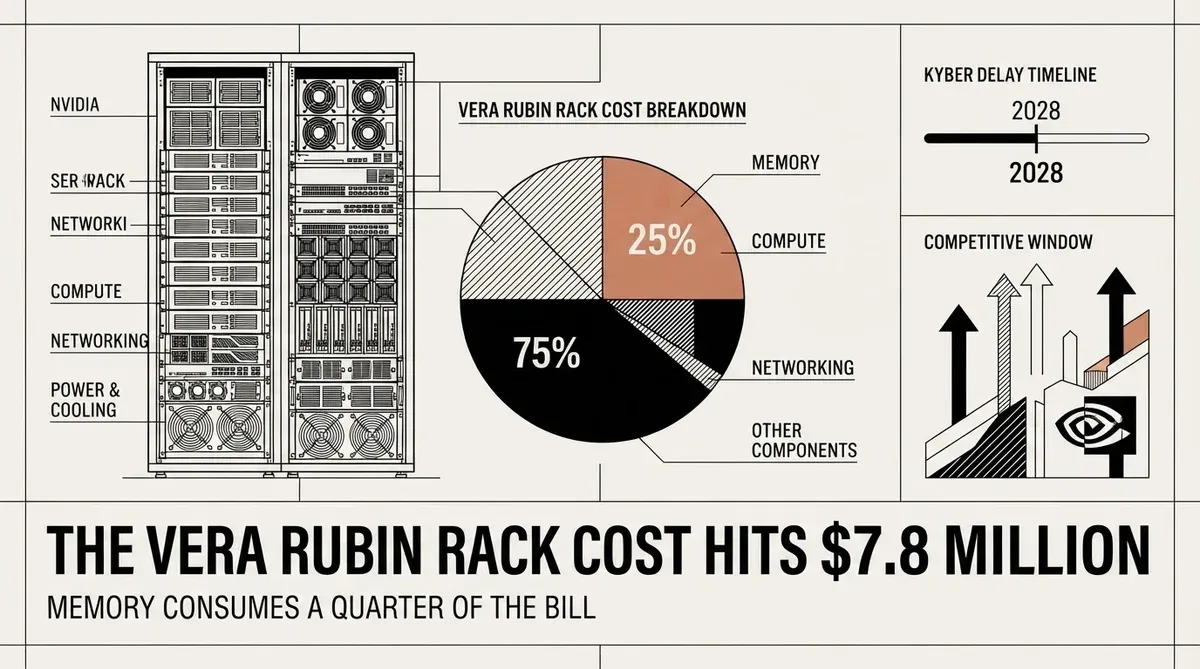

The Vera Rubin Rack Cost Hits $7.8 Million as Memory Consumes a Quarter of the Bill

The Vera Rubin generation from Nvidia is a structural shift in AI infrastructure economics that hyperscalers are only beginning to price correctly. The Vera Rubin rack cost now stands at $7.8 million for the VR200 NVL72, nearly double the $4 million price of the GB300 generation, according to Morgan Stanley estimates. But the headline number is less interesting than what drives it. Memory now consumes a quarter of the bill of materials, up from a low single-digit share in previous generations, and that single change upends the procurement logic that hyperscalers have relied on for years.

Driven by larger LPDDR5X capacity and 3D NAND storage, memory now costs about $2 million per rack — a 435% increase from the prior generation. During the GB300 cycle, memory accounted for 5–10% of the total BOM. Now it sits at 25 to 30 percent. The GPU share, meanwhile, has fallen from 63 percent to 51 percent. The takeaway is direct: the center of gravity in AI infrastructure spend is migrating away from compute silicon toward memory. That has consequences for how deals get structured, how supply chains get managed, and where the leverage sits in vendor negotiations. The implication is clear: memory cost is no longer a fixed overhead in compute-unit economics but a primary variable that hyperscalers must manage actively.

Morgan Stanley also highlights a practical implication that procurement teams should take seriously. Memory supply constraints now warrant the same scheduling attention as GPU allocation. The structure of procurement alone can move final pricing by more than $1 million per rack. When a single decision about sourcing strategy can swing the cost of one rack by seven figures, the margin for error in supply chain planning shrinks dramatically. This is a new variable in a procurement equation that was already complex.

Why the Vera Rubin Rack Cost Is a Procurement Game-Changer

The cost story is significant, but the roadmap gap may prove more consequential in the medium term. Nvidia's Kyber NVL144 rack, designed to pair with the Rubin Ultra GPUs expected in 2027, has slipped to 2028, according to analysis from SemiAnalysis. The delay exceeds 12 months. The technical holdup is in PCB midplane manufacturing, which requires connecting eight Oberon racks into a single cabinet architecture. Nvidia also canceled the NVL72x2 stopgap that would have bridged the gap, leaving no proven path to scale Rubin Ultra capacity in 2027.

Nvidia has stated that its roadmap is intact, and schedule pressure is nothing new in hardware development. But the absence of a validated scaling path for 2027 matters when competitors are offering alternatives. The delay opens a window for rival suppliers to capture hyperscaler spend that would otherwise have gone to Nvidia's next-gen rack ecosystem. When a single rack costs $7.8 million and memory procurement alone can shift budgets by more than a million dollars, the elasticity of infrastructure budgets becomes a strategic factor for Nvidia's competitors to exploit.

Memory Supply Chain Gains Strategic Weight

Samsung Electronics has already begun mass production of its most advanced data center storage drives for the Vera Rubin platform, as Bloomberg reported this month. That signals that Nvidia is moving toward production readiness on the core platform even as the high-end rack architecture encounters delays. But it also underscores the new centrality of memory suppliers in AI infrastructure. When memory accounts for a quarter of system cost, Samsung and its competitors become as strategically important as TSMC in the AI supply chain. The memory vendors are no longer peripheral players supplying commodity components. They are structural participants in the cost profile of every AI rack.

This shift has implications for contract terms and pricing leverage. In the GB300 era, a hyperscaler negotiating GPU pricing would view memory as a secondary line item, important but not the driver of total cost. In the VR200 era, memory cost is large enough and variable enough that it demands its own negotiation track. Procurement teams that treat memory pricing with the same rigor they apply to GPU pricing will have a structural advantage. Those that bundle memory procurement into the same process without dedicated focus risk leaving millions on the table per rack purchase.

A New Procurement Discipline

For years, AI infrastructure buyers optimized primarily around GPU availability. They planned lead times around wafer starts at TSMC and CoWoS advanced packaging capacity. The Vera Rubin rack cost structure forces them to add memory to that critical path. LPDDR5X provisioning and NAND storage allocation now carry the same weight as GPU allocation in the cost equation. The financial swing from getting those decisions wrong is measured in millions per rack.

This is not just a theory. Morgan Stanley's estimate that procurement structure alone can move pricing by $1 million per rack is based on the specific dynamics of memory supply. Memory is a more commoditized market than GPUs, with different pricing mechanisms, different lead times, and different supplier concentration. Understanding those mechanics, and building the negotiation leverage to exploit them, is a new competency that hyperscalers must develop or buy.

The companies placing the largest bets in AI infrastructure (Microsoft, Meta, Google, Amazon) are now operating in a market where a single rack costs nearly $8 million and the next scaling architecture is at least 18 months behind schedule. The Vera Rubin rack cost demands a more deliberate procurement approach than the Hopper and Blackwell eras required, when the GPU was the dominant cost driver and memory was a rounding error. The penalty for haste is now measured in millions.

The Competitor Window

The Kyber delay to 2028 creates a window that Nvidia's competitors are poised to exploit. AMD, Intel, and custom ASIC makers all have incentives to position their architectures as alternatives for hyperscalers who need to expand capacity in 2027 but cannot access Rubin Ultra at scale. The Vera Rubin rack cost of $7.8 million per unit already creates a high bar for ROI justification. If buyers also face uncertainty about the upgrade path beyond Vera Rubin, the case for diversifying suppliers becomes stronger.

The counterargument is that Nvidia's software ecosystem and installed base create switching costs that protect its position. But switching costs are easier to overcome when the alternative is a $7.8 million rack with uncertain upgrade timing. The hyperscalers with the largest AI buildouts are sophisticated enough to run multi-vendor environments. The Kyber delay gives them a reason to accelerate those diversification plans.

Why this matters

The Vera Rubin generation is the moment when memory costs stopped being a footnote in AI infrastructure budgets and became a primary line item. Combined with the Kyber delay, hyperscalers face a cost structure that demands new procurement discipline and a roadmap that offers fewer scaling options than expected. The hyperscalers that treat memory sourcing with the same rigor they apply to GPU allocation will capture a cost advantage that compounds over the next two years. Those that don't will pay a seven-figure premium per rack for the privilege of learning the lesson late. For Nvidia's competitors, the alignment of high per-rack costs and a roadmap gap creates the best window to capture infrastructure spend since the AI buildout began.

AI-generated image.

Related Articles

- NVIDIA Debuts Vera Rubin Architecture to Slash AI Inference Costs

- NVIDIA Revenue Surges to $81.6B as New Vera Rubin NVL72 Architecture Targets Agentic AI Efficiency

- NVIDIA Vera Rubin Platform Powers New Dell Servers to Slash AI Costs

✔Human Verified

Researched and cross-referenced against primary sources by the Bytevyte editorial team.